THE CFD HUB

06 May 2026

A new data-crunching tool - the CfD Hub - has been created which sheds fresh light on a vexed question: are renewables cheap?

Screenshot from the CfD Hub.

These Islands has been writing about this issue for a long time. We have generally argued that CfD strike prices, adjusted for inflation into today’s money, represent the best measure of the true cost of renewables.

Strike prices emerge from reverse auctions1In other words: the lowest bid wins, which happen every year or so in Allocation Rounds.

The auctions have dedicated pots for each generation technology, and the strike price sets the guaranteed price for output (uplifted each year for inflation) which gives developers the certainty they need to finance and construct the project.

The standard contract length was 15 years in Allocation Rounds 1-6, and was upped to 20 years in Allocation Round 7, which happened in January/February 2026.

Nothing gets built without first securing a CfD. So there is a perfectly sound argument for the Allocation Round 7 strike price secured by (for example) offshore wind being a true reflection of the current cost of offshore wind. It’s the guaranteed price for output (over 20 years) which the latest generation of offshore wind farm projects need today to proceed to construction.

But it should be clear that this doesn’t tell us the whole story. The generation assets operating today are a mixture of projects which secured CfDs in earlier Allocation Rounds (the first of which concluded in 2015) and even older projects subsidised under a predecessor scheme - the Renewables Obligation.

Setting aside (for now) the Renewables Obligation projects, it would be useful to calculate (for any particular generation technology) the average strike price of assets which currently exist. And to get an idea of how this average will evolve as capacities from more recent Allocation Rounds come on stream.

This is what the CfD Hub allows you to do, as well as to filter the projects by GB nation and to visualise the data on a map. Plus a whole lot more besides - I would encourage readers to have a play with the tool to discover everything it can do.

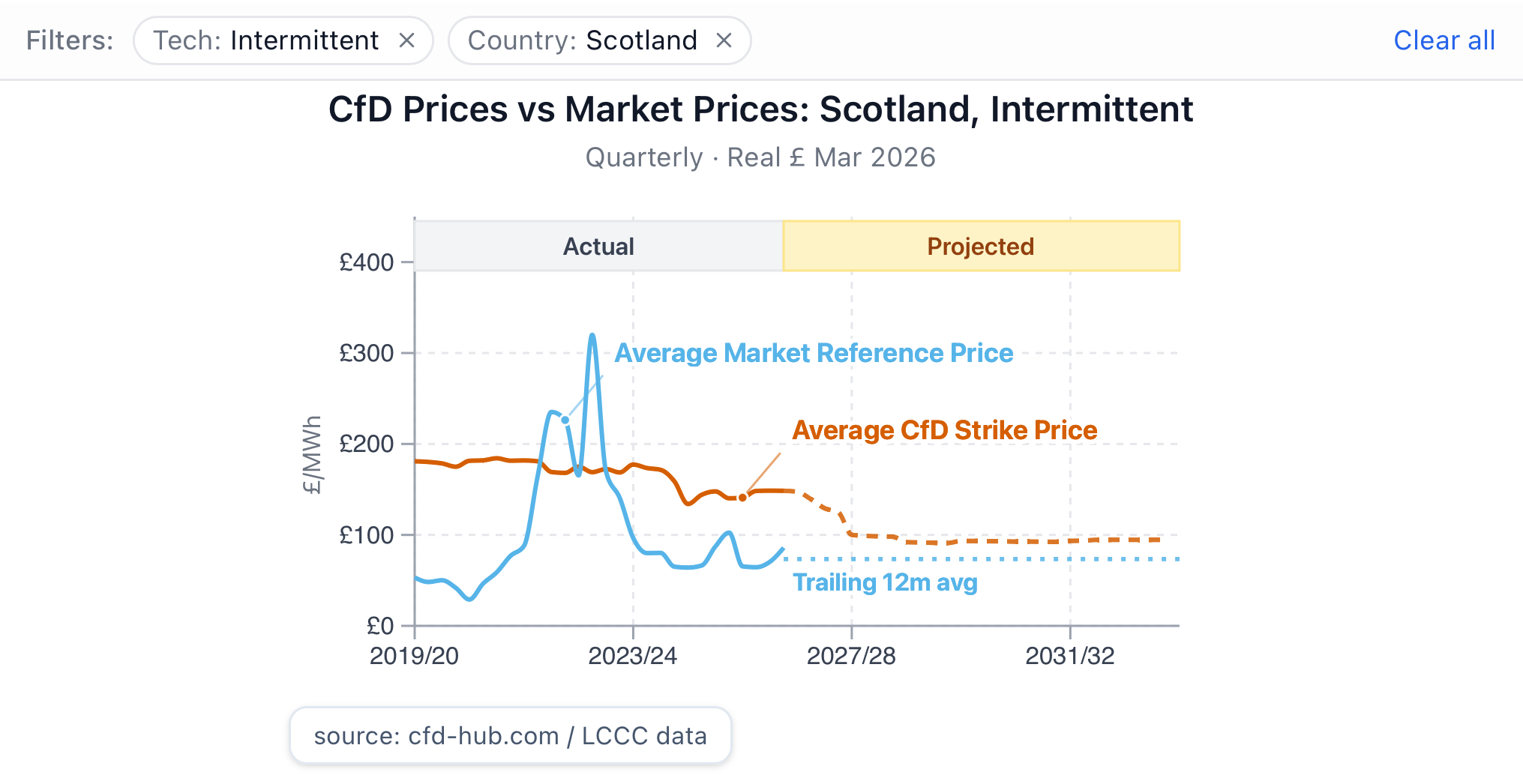

The chart below shows the average strike price data filtered for intermittent (ie renewable) projects in Scotland. For historic years the average is weighted by actual output, and for future years it is weighted by a projected level of output based on NESO load factor assumptions.2https://www.neso.energy/document/376346/download

If you experiment with the various filtering options, you will find that there isn’t really a huge difference in average CfD strike prices by GB nation. But since the cheapness of Scottish renewables is a politically loaded question in the current election, this discussion will focus on Scotland.

The story told by the above chart should be familiar to anyone who has followed the CfD Allocation Rounds.

Strike prices were relatively high in round 1, somewhat lower in round 2, and then rounds 3 and 4 cleared at very low prices - unrealistically low, as it turned out. Rounds 3 and 4 took place when inflation was benign and interest rates were ultra-low. That world no longer exists and many of those projects have since been scaled back, re-bid in subsequent rounds, or completely cancelled.

Round 5 was a partial failure: the price cap below which developers had to bid for offshore wind was set too low, resulting in no CfDs at all for offshore wind in that auction.

And then rounds 6 and 7 saw steadily rising prices and large amounts of capacity being procured, as the incoming Labour government pressed ahead with its Clean Power 2030 plan. The increased strike prices in rounds 6 and 7 were caused by higher raw material costs and an increased cost of capital - that is higher interest rates.

The orange line in the chart perfectly reflects this story: it starts out close to £200/MWh and gradually declines as lower priced capacity comes on stream. There is enough still in the pipeline from rounds 3 and 4 to pull the output-weighted average down from recent levels of £150/MWh to about £100/MWh by 2027/28.

And then the large amounts of capacity from rounds 6 and 7, which won’t come on stream until the early 2030s, will see the average settle down in Scotland at around £95/MWh, in today’s money.

But because of the inflation indexation built into these contracts, the output-weighted average strike price of CfD-supported Scottish renewables will, by the 2030s, be well above £100/MWh.

Now look at the blue line on the chart. This is the wholesale market price of electricity - the reference price for CfD support. If the wholesale price is above the strike price, generators pay back to the system. But when the wholesale price is below the strike price, generators receive top-up payments at the levels required to deliver their guaranteed CfD remuneration.

With the exception of the period immediately after Russia’s full-scale invasion of Ukraine, CfD-supported Scottish renewables have always been priced above the wholesale market price. In other words: CfD-supported Scottish renewables have almost always cost consumers more than the gas-linked price of electricity.

Those costs are quantified at an aggregate level and by GB nation in the following table:

Two things are notable:

Firstly: CfD-supported renewables in Scotland receive very substantial top-up payments, over and above the gas-linked wholesale price of electricity. Net payments to Scottish projects in the 2025/26 financial year totalled nearly £500m.

And secondly: Scottish projects received 16% of GB-wide net payments in 2025/26. This is important because those top-up payments are fully socialised across GB bill payers. In other words: Scottish projects created 16% of the net CfD top-up costs in 2025/26, but Scottish bill payers only shouldered a population share (ie ~8%) of the total CfD top-up burden.

The Renewables Obligation

Before the CfD regime took over, renewables were subsidised under a different scheme - the Renewables Obligation. This closed to new capacity in 2017, but many wind farms are still operating today under this legacy scheme.

Rather than guaranteeing a fixed price for output, the Renewables Obligation issued, over the first 20 years of an asset’s operating life, a certain number of Renewables Obligation Certificates (ROCs) per MWh of output. The exact number of ROCs depended on the generating technology, with onshore wind receiving around one ROC per MWh.

ROCs have a value which today stands at about £69. This cost is fully socialised, historically through customer bills, and more recently (in part) through general taxation.

So a ROC-supported wind farm does not have the same revenue certainty as a CfD-supported wind farm. But the developer does know that for 20 years, per MWh, it will get whatever the wholesale market price of electricity is, plus (for an onshore wind farm) the value of one ROC.

Much ROC-supported capacity (principally onshore wind) will be reaching the end of its 20-year period of support over the coming decade. There is considerable uncertainty over what will happen to these wind farms as they enter the so-called “merchant tail” of their operational life.3Katrina Salmon and Michael Grubb at UCL have done some interesting work on this question.

This uncertainty at least partly explains the UK government’s recent announcement of a new class of CfD - the Wholesale Contract for Difference (WCfD)4https://www.gov.uk/government/news/decisive-action-to-break-influence-of-gas-on-electricity-prices - which will provide some level of revenue certainty for ROC-supported capacity entering its merchant tail.

Wind turbines typically last for about 25 years. Perhaps 30 years, if you are lucky. So the merchant tail is a short period compared to the 20 years of ROC support.

WCfD strike prices will certainly be lower than the strike prices for new capacity, and will therefore be helpful in exerting downward pressure on bills (although only modestly - CfD volumes will dominate the generation mix).

But these will be “cigar butt” prices, eked out of assets in their twilight years. They will not reflect the true economic costs of those assets.

Which is a roundabout way of explaining why the CfD Hub does not include ROC capacity. The merchant tails of ROC-supported wind farms do matter, but they need to be thought about quite separately.

Please log in to create your comment